How Loan Apps in Kenya Can Trap You in Debt and What to Do

In Kenya, digital loan apps have become a quick solution for people needing instant cash. While these apps offer convenience, they often come with high interest rates and short repayment periods that can quickly trap borrowers in a cycle of debt.

What Are Loan Apps in Kenya?

Loan apps in Kenya are mobile applications that allow users to borrow money instantly without collateral. Money is usually disbursed directly to your M-Pesa account, making it convenient for emergencies. Popular apps include Tala, Branch, and Zenka.

Why Loan Apps Became Popular in Kenya

- Quick access to cash without paperwork

- No collateral required

- Instant disbursement via M-Pesa

- Accessible to people without bank accounts

The Hidden Debt Trap Behind Digital Loans

While the convenience is appealing, many borrowers underestimate the interest rates and the short repayment timelines. Some users end up borrowing from multiple apps to repay previous loans, creating a dangerous debt cycle.

Signs You Are Stuck in Loan App Debt

- Borrowing new loans to pay off existing loans

- Using over 30% of your salary to repay loans

- Receiving multiple repayment reminders daily

- Feeling stressed about upcoming payment deadlines

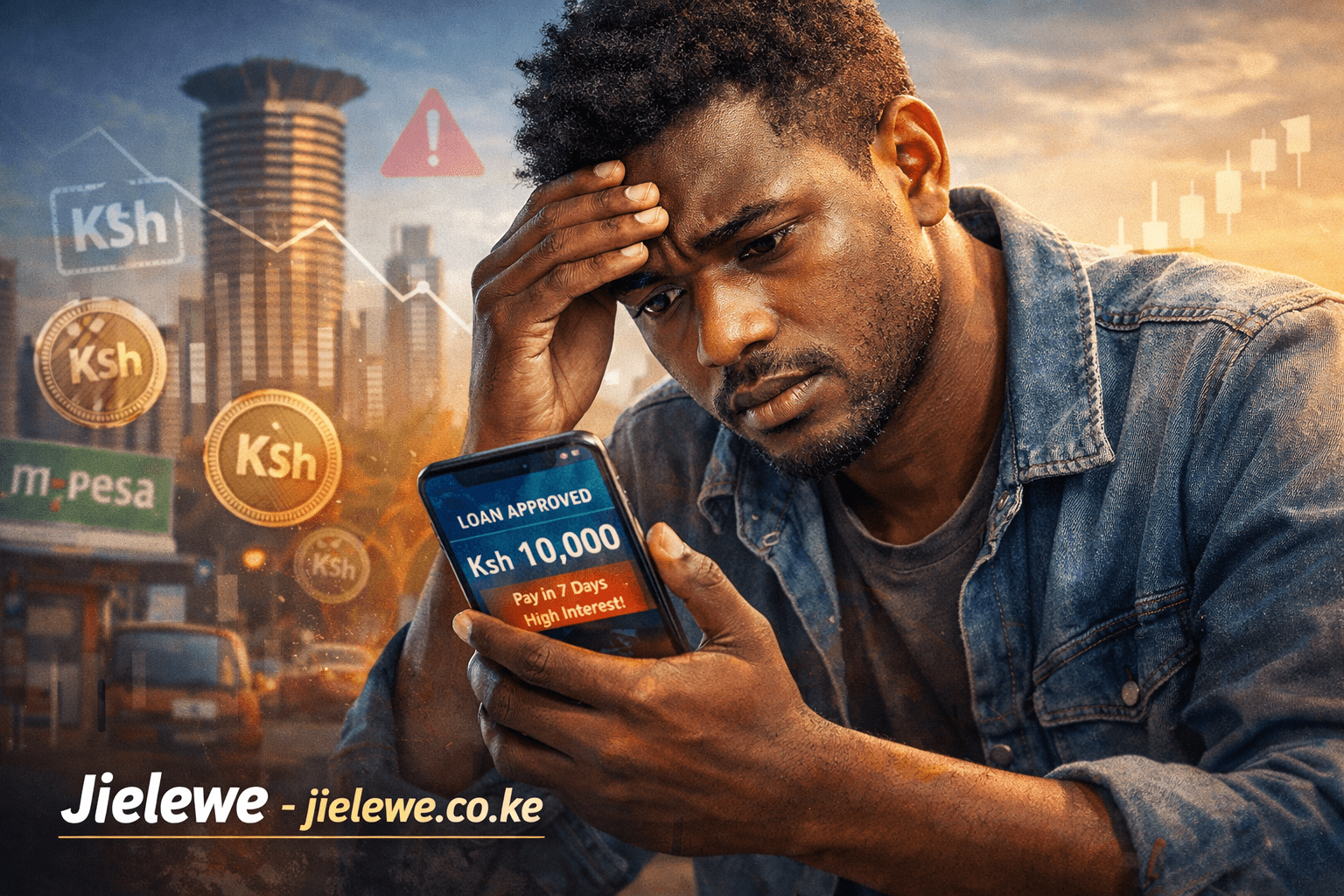

Real Example of a Loan Debt Cycle in Kenya

For example, a borrower takes a KSh 10,000 loan at 15% interest per month. When repayment is due, they may not have the cash and take another KSh 10,000 loan from a different app. The cycle repeats, causing the debt to grow rapidly.

Why High Interest and Short Repayment Periods Are Dangerous

- Exponential growth of debt if unpaid

- Difficulty in budgeting monthly expenses

- Risk of default and negative credit reporting

- Emotional stress and financial instability

How to Escape the Loan App Debt Trap

To escape, start by creating a realistic repayment plan. Prioritize paying off high-interest loans first, and avoid taking new loans. Communicate with lenders if you cannot pay on time.

How Budgeting Can Stop the Debt Cycle

Effective budgeting is essential. Tracking every expense helps you identify areas to cut costs. Apps like Jielewe allow you to monitor your spending and prevent overspending, making it easier to pay off loans on time.

Tools That Help You Track Spending

Besides Jielewe, keeping a manual expense log or spreadsheet can help, but digital solutions are faster. Use budgeting tools to categorize spending and identify unnecessary expenses.

Loan Apps vs Traditional Bank Loans

| Feature | Typical Loan Apps | Traditional Bank Loans |

|---|---|---|

| Approval Time | Minutes | Days to Weeks |

| Collateral Required | None | Often Required |

| Interest Rate | High | Lower |

| Repayment Period | Short (7-30 days) | Medium to Long |

If you want a deeper understanding of budgeting, saving, and financial planning, read our complete guide to personal finance in Kenya.

Key Takeaways

- Loan apps provide fast cash but can trap borrowers in high-interest debt.

- Short repayment periods and borrowing multiple loans increase risk.

- Tracking spending is essential to avoid falling into a debt cycle.

- Apps like Jielewe can help monitor expenses and plan repayments.

- Responsible borrowing and budgeting prevent financial stress.

Conclusion

Digital loans are useful in emergencies, but understanding the risks is critical. By monitoring your expenses, creating a repayment plan, and using tools like Jielewe, you can avoid falling into the loan app debt trap and improve your financial health.

Frequently Asked Questions

Are loan apps legal in Kenya?

Yes, many digital lenders operate legally under regulations set by the Central Bank of Kenya.

Why are loan apps dangerous?

High interest rates, short repayment periods, and easy access can trap borrowers in cycles of debt.

How can someone escape loan app debt?

Create a repayment plan, prioritize high-interest loans, avoid taking new loans, and track spending carefully.

What interest rates do loan apps charge?

Loan apps often charge high monthly interest rates, sometimes exceeding 10–15% per month, depending on the lender.

How can budgeting help avoid loan debt?

Budgeting helps track income and expenses, making it easier to save for emergencies and avoid borrowing from loan apps.